Managerial Accounting –Decision Making: Relevant Costs & Benefits

When you have a choice between two or more alternatives and you have to select one, you are making a decision. If there is no choice, you will have to simply follow or obey. So a decision implies a selection, a choice, a verdict or a nod.

In everyday life, decisions are made. A personal decision affects an individual but organizational decisions cause a change, good or bad, to a lot many people known as stakeholders. So decision making in an organization must be systematic and not off the cuff. A good executive must be good at decision making.

DECISION MAKING

A formal definition of decision making by Wikipedia.org is given below:

Decision making can be regarded as an outcome of mental processes leading to the selection of a course of action among several alternatives. Every decision making process produces a final choice. The output can be an action or an opinion of choice.

It may be noted that every decision involves a certain degree of risk. Very few decisions are made with absolute certainty. So a good decision would be to choose a solution with the highest probability of success and in accordance with the goals, desires, lifestyle and values etc.

RELEVANT COST AND BENEFITS

Relevant means linked or concerned. If an event has nothing to do with a situation, it is not relevant. Marble processing units at Karachi may suffer because of unrest in a far-off area like Swat. It would be relevant as Swat supplies marble rocks. But turmoil in Hyderabad, a town much near to Karachi than Swat, would be irrelevant for the marble units.

Any decision must be evaluated under cost-benefit criteria. The benefits must be more than the cost except in social projects where benefits may be equal to cost. Benefits can be in the form of cash return, perks, advantages, customer’s satisfaction or reputation of a company. While cost means value, worth or sacrifice made.

Only relevant cost should be considered. CIMA defines relevant costs as: ‘the costs appropriate to a specific management decision’ A study of relevant costs and benefits helps make better decision?

Six steps in decision making process and MA role

- Clarify the decision problem. One must be clear about the problem. One must look for the root cause or hidden problem rather than the apparent problem. Some skill is required to define a problem in such terms that can be addressed effectively.

- Specify the criteria. After clarifying a problem, criteria must be specified for decision-making. What is the objective: maximize profit, increase market share or social service.

- Identify alternatives. Explore all alternatives, their pros and cons. This is a critical step in the decision making process.

- Develop a decision model. This is a simplified version of the problem. No irrelevant information, only factors relevant to the problem are highlighted. It brings together all elements of a problem like the criteria, the constraints, and the alternative.

- Collect the data. Relevant data must be collected to incorporate objectivity in the process. It may be primary data or secondary data. But it must be up-to-date, timely and accurate.

- Select an alternative. One all formalities are completed, requisite information obtained and processed, a most suitable or appropriate choice should be selected.

Qualitative and Quantitative Analysis

Management Accountant mostly deal with financial data. But they also maintain records of physical units produced and quantities of raw material consumed, labor hours used. In addition, they asses qualitative factors such as employee morale, customers satisfaction, image of the company in the eyes of the public.

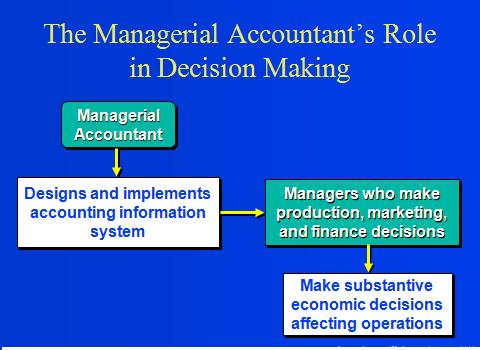

Role of Management Accountant

A management accountant is a member of cross functional team and, having unrestricted access to MIS, makes a contribution by providing facts and figure which bring objectivity to the report.

Besides, a management accountant would ensure that the information must be relevant (pertinent to the decision problem); accurate (precise); and timely (arrive in time for the decision to be made). Companies will occasionally trade-off accuracy for timeliness.

Relevant Costs

In order to qualify for relevancy, a cost must meet two criteria: (i) They affect the future and (ii) they differ among alternatives.

Normally, the following are relevant Costs:

DIFFERENTIAL COST

- A differential cost is the difference in cost items under two or more decision alternatives specifically two different projects or situations. Where same item with the same amount appears in all alternatives, it is irrelevant. For example, a plot of land can be used for a shopping mall or entertainment park. The plot is irrelevant since it would be used in both the cases. Similarly, future costs and benefits that are identical across all decision alternatives are not relevant.

- An example of differential cost would be of a company which is selling its products through distributors. It is paying them a commission of Rs.16 million. Any alternate which costs lesser would be considered. Let us suppose that the company is planning to appoint salespersons to sell its products and cancels the contracts with distributors. In this case, the selling expense is expected to be to Rs.12 million. There is cost differential Rs.4 million (Rs.16 m - 12m). This a good sign but the risk would have to considered for changing the channel of distribution. If there is low risk, it would be prudent to go for own arrangements for sales.

- Differential costs must be compared to differential revenues. In case, switching over to direct sales bring additional revenues of Rs.2 million, it would increase the net benefit to Rs.6 million. This would provide more comfort to the decision maker while considering a change in the distribution channel.

INCREMENTAL OR MARGINAL COST

- Whereas differential cost is a difference between the cost of two independent alternatives, incremental or marginal cost is a cost associated with producing an additional unit. In case of a university, it could be cost of admitting another student. Even operating a second shift is an example of incremental cost. It would be noted that the two decisions are not independent as second shift depends upon first shift.

- Increamental cost must be compared with incremental revenues to arrive at a decision.

OPPORTUNITY COST

- It is cost of opportunity foregone. Mr. Ahmed Shah left a bank job which was paying him Rs.15,000 per month and got admission in a University. Monthly fee-charge in the university is Rs.10,000 per month. For Ahmed Shah, this would be Rs.25,000 per month (Rs.10,000 + Rs,15,000).

- Farhana is a fresh graduate from a business university. She got two offers, one of Rs.25,000 from an investment bank and another of Rs.15,000 for a teaching-assistant in a university. Another of her class-fellow, Shabana got the same offer from the same university. While Shabana would be happy to join the university, Faraha would not be as she would lose an opportunity to serve at the bank for Rs.25,000.

- Whenever an organization is deciding to go for a particular project, it should not ignore opportunities for other projects. It should consider (i) what alternative opportunities are there? (2) Which is the best of these alternative opportunities?

IRRELEVANT COSTS

Sunk costs are past costs. These cannot be changed with any future decision. Suppose, a piece of land has already been purchased by a company for a sum of Rs.30 million. Also suppose, the company is consider covering it with a wall which would cost Rupees two million. While the sum of Rs.30 million is a sunk cost, the other of Rs.2 million is a future cost or out of pocket expenses. It is relevant to decision: whether to erect a wall now or postpone it for the next month, whether it should be two-meter or three-meter high. Whether a wall is erected or not and, if erected, whether it is 2 or 3 meter, the sum of Rs.30 million for land would remain the same. It is a sunk cost and therefore irrelevant to the decision.

Similarly, a cost which is identical in all decisions is irrelevant.

Special Decisions

There are special decisions where relevant costs and benefits are to identified before proceeding further. Such decisions are:

- Accept or reject an order when there is excess capacity

- Accepting or reject an other when there is no excess capacity

- Outsource a product or service

- Add, drop a product, service or department

- Sell or process further

- Optimization of limited resources or working under constraint.

SUMMARY

Management Accounting picks up data from cost database and prepare reports for the management to facilitate decision making. Both financial and non-financial data are used in the reports. In the non-financial data, both numerical and non-numerical information are used.

While numerical information consist of operational statistics such as units produced, raw materials considered and labor hours used, the non-numerical or qualitative information pertain to customers satisfaction, employees moral, access to markets and image of an organization.

For a particular decision, different types of cost and benefits are considered. Called relevant costs, these have a bearing on the future and differ under various decision alternatives. If any of these qualification is absent, it would be an irrelevant cost.

Since most decision are under uncertainty, some other techniques are used to given an insight in the problem such as best- worst case scenario, sensitivity analysis and simulation.

Though technology has made a lot of advancement in manufacture, concepts like cost : benefit analysis are still valid and useful. They have been made more strong and convincing with the introduction of ABC, ABM and EVA.

Comments

markman1914@gmail.com on February 28, 2016:

thank u so much sir,

sir r puting ur great effort just for our future......i am really thankful to u sir

sammy o howbay on May 14, 2015:

Good morning Sir,

I'm Sam from Nigeria and I'm involving in accounting Higher National Diploma programme. I have a paper which I'm to present on the Relevance of ICT to decision making processes: the accounting perspectives. Could you help me out how I'll go about it

sheik mahaboob basha on December 01, 2014:

thanku very much sir

hafeezrm (author) from Pakistan on November 05, 2014:

Thanks Tariq Baig. I am in Bahria University, Karachi as a visiting faculty.

Hafeez Sahib on November 05, 2014:

I was searching you . How are you sir.

Tariq Baig

zeni on October 24, 2014:

Thank you

frank itambiko on September 29, 2014:

thank you very much sir you open my mind well.

Elvis keya on July 12, 2014:

the article has opened my mind congratulations

Ahadi on June 23, 2014:

I appreciate your thought in this article keep coming up.

@NanaBoatengSkab on May 20, 2014:

sir, what are the various costs used in decision making and their characteristics?

summan azam on May 08, 2013:

give some references of articles that are related to relevant costing application in manufacturing conerns.impacts of relevant costing principles

aaa on April 30, 2013:

This is full of water when anyone start to drink it.it shows how depth it has

thanks for this effort to us

imty from int islamic university on April 04, 2013:

hi,,sir

can i have exercise solution"s web site id..

tnx

Mr MW Mapaya on March 08, 2013:

I respect your Capacity in Cost and Management respective, i can proudly declare that am future accountant, it’s in deed fair for cost manager to focus on qualitative and quantitative characteristics, which will boost the company's sustainability in long run. Keep up with good work of boosting organization to succeed

hafeezrm (author) from Pakistan on February 15, 2013:

Please surf the Internet. There are lot many information.

Krystian on February 15, 2013:

Could You recommend me simply but reliable literature about relevant cost? I write in Poland thesis about relevant cost in decison-making. Thanks for your help.

Silas on February 05, 2013:

sir

I want you to throw more light on liner programming & decision tree in management accounting.

hafeezrm (author) from Pakistan on January 21, 2013:

In-source and out-source are two opposite terms. In-source mean using own facilities for some out-side jobs. For example, a bank has a large IT Division and feels the IT equipment and staff is not being fully utilized. There are many options such as (i) staff reduction or (ii) in-sourcing which means getting outside jobs to do in house. When there is an idle capacity, in-sourcing is recommended.

vipul on January 21, 2013:

sir

what is the meaning and difference between insource and outsourcing decision in Management Accountancy Decision making

hafeezrm (author) from Pakistan on January 03, 2013:

Of course, it matters. Many aspects are difficult to quantify and hence qualitative terms are used like reputation, goodwill, quality of employees, customers dedication, suitability of location and thousand others.

jasnta on December 27, 2012:

Could you please help me to get the answer of below question

'' does qualitative analysis matter in managerial decision?''

Suhel on October 02, 2012:

Dear Sir,

Thanks a lot.

Regards

hafeezrm (author) from Pakistan on October 01, 2012:

Definition is given in the hub. Financial accounting is in aggregates say sales during 2011. A decision to drop a product for poor sales or to encourage a product for showing good result cannot be made unless one knows contribution of each product in total sales for the past 2 or 3 years. This contribution is given Cost Accounting and a decision is taken by Management Accounting.

Suhel on October 01, 2012:

Dear Sir,

Could you please help me to get the answer of below question.

"Define the importance of accounting as a tool of managerial decision-making. How is management accounting different from financial accounting?

hafeezrm (author) from Pakistan on August 02, 2012:

ROCE will down. But some other related ratios would improve giving a good impression on the company;s image. Such ratios are: fixed assets cover, fixed assets to total assets and solvency)

Habib on July 18, 2012:

Sir Pls anser the Q

A company has revalued its non-current assets during the most recent accounting period. How will this affect the calculation of return on Capital Employed (ROCE) ?

shwetha on July 05, 2012:

Dear sir

thank you very much add some more information in this regard.

lizore on June 20, 2012:

nice article! clear & well understandable

dharmmelorlah on June 18, 2012:

I will say a one thousand and one thank to this site for solving my question for me, is it for my assignment in class, question from lecturers and frd and most especially on my project.

Thanks.

hafeezrm (author) from Pakistan on June 09, 2012:

I am on my annual safari. Please consult a book on managerial accounting.

Aliyu on June 09, 2012:

Kindly provide me materials that concern solving questions under certainty,uncertainty,risk,relevant cost ,etc

hafeezrm (author) from Pakistan on May 05, 2012:

Thanks Roxy for reading my article. You may go through this link for further knowledge:

http://www.microbuspub.com/pdfs/chapter2.pdf

roxy on May 05, 2012:

sir, do you have any detailed article on the special decisions part?

hafeezrm (author) from Pakistan on May 04, 2012:

Thaks Joy Lucky and Roxy for your comments.

roxy on May 04, 2012:

article helped a lot. thanks XD

Joy lucky on May 03, 2012:

Thanks Sir.u hv really helped me.pls sir,can u tell me in details The threats to the relevant management accounting and how they can be integrated.thanks

hafeezrm (author) from Pakistan on April 22, 2012:

@VERA

Cost accounting tries to find out true cost of a product. If a product is loss-making, it evident from product-wise profit and loss account. If there is no hope of improvement, it should be discontinued. Of course sometimes, a project appears loss-making due to wrong costing. ABC and EVA are refined methods to arrive at true cost of a product.

vera on April 22, 2012:

may i ask, how to know whether a product need to continue or discontinued to produce based on standard costing and relevant costing? Is that we need to compare the actual and forecast result?

hafeezrm (author) from Pakistan on April 20, 2012:

Thanks Renaissance for your comments.

Renaissance on April 20, 2012:

That was wow! now as i sit for ma exams nothing to fail

hafeezrm (author) from Pakistan on April 15, 2012:

Thanks Imran.

imran on April 15, 2012:

salam... sir ap bohat mushkil topic ko bhi asan words mai bata daty hain thanks... ap ki waja sy bohat help milti hai q k mai self study kar raha hon.... once again thanks a lot. plz aisay he apny students ko guide karty rahye ga. allah pak apko is ka ajar day ameen. imran

hafeezrm (author) from Pakistan on March 27, 2012:

@Blessing, thanks for your comments. God bless you.

Blessing on March 26, 2012:

Pls i want 2 be part of u

hafeezrm (author) from Pakistan on March 20, 2012:

Briefly speaking, management accountant is a part of management which is involved in decision-making. As a management accountant has access to all accounting and cost information, both financial and non-financial (Quantitative production & sales), he or she can provide background information necessary for decision-making.

miss yuka on March 20, 2012:

sir,

may i know the ways in which a management accountant might contribute to a formal decision making process?

hafeezrm (author) from Pakistan on March 18, 2012:

Thanks Muddasir Aliya for your comments.

muddasir Aliyu on March 18, 2012:

thank so much sir may continue help you

hafeezrm (author) from Pakistan on March 10, 2012:

Thanks Shannon and John Ouko Otok for your comments.

John Ouko Otok on March 09, 2012:

The information provided in this section concerning about Relevant cost revenue and decision making is quite informative and relevant to the data being provided in most Universities. The only issue at hand is that there is no information concerning the major methods used when an individual(s) wants to carry out an effective decision regarding the best alternative that might eventually assist in the attainment of the major objectives of an Organization. I loved the article though. Cheers

Shannon on February 28, 2012:

Thank you for your help!

hafeezrm (author) from Pakistan on February 26, 2012:

Cost Accounting in fact is a data base. This is used to compute reports based on actual cost of product or a process or a department. Side by side, standard cost for each product or process or department is computed. This is compared with actual to find out variances which may be due to internal or external factors.

This being the background, it would help the business in its future decisions: what products to promote, what to delete, which manager to reward, which to penalize, which branch to close, which to upgrade.

There are endless decisions based on (i) cost accounting, (ii) company's conditions, (iii) industrial environments and (iv) vision.

Ukoh Blessing on February 26, 2012:

Thank u sir, your article was a great insight. Please sir can you discuss something on:

cost accounting as a guide to futuristic decision

linda on February 20, 2012:

thank u sir, your article helps me a lot.

hafeezrm (author) from Pakistan on February 17, 2012:

Process costing is suitable for industries engaged in mass production of near identical products.

Please go to the given and find answer to your question:

https://hubpages.com/education/Managerial-Accounti...

jyoti narvekar on February 17, 2012:

U have written a great article

Could you just help me out in answering how does process costing helps management in decision making?

could u just answer me in detail sir.

hafeezrm (author) from Pakistan on February 16, 2012:

@Richie Ehimare .o.

I am not aware of the derivation of cost accounting. However, my comments on code of cost accounting are as follows.

In cost accounting, one has to deal with Direct Costs (Direct Material and Direct Labor) and Manufacturing Overhead. The latter is called a common cost and has to be shared by various products or process. It poses a problem of allocation or assignment. With the help of cost code for each expense, using alphabetic or numerical method, this allocation is facilitated.

Richie ehimare .o. on February 16, 2012:

Tank u very mush sir it gud 2 av people like u. I wish 2 b like u. Sire wat are the derivation of cost accounting and the code of cost accounting?

hafeezrm (author) from Pakistan on February 15, 2012:

@Obinna Christian,

Consider cost accounting as database or MIS. It helps generate data for business decisions such as which product to promote, which one to drop. Besides information provided is used in managerial evaluation by comparing projected performance with actual ones ultimately leading to promotions and demotions.

Please ask any specific question.

Obinna Christian on February 15, 2012:

Am an Accounting student, please, what are the objectives and importants of cost Accounting to managerial decision?

hafeezrm (author) from Pakistan on February 12, 2012:

Thanks Chukwuemeka Victor for your comments.

Chukwuemeka Victor on February 12, 2012:

Sir, tank u so much 4 dis wonderful article, u ar simply Great. All grease 2 ur elbow. Sir am a marketin student in fidei poly, i need ur counselin and professional advices concernin my course of study.

hafeezrm (author) from Pakistan on February 06, 2012:

Thanks MUH for your message.

MUH on February 06, 2012:

Hello My name is Mohammed and I am promising research on the role of the accountant in administrative costs in order to rationalize the decision-makincosts in order to rationalize the decision-making in industrial companies and suffer from the problem of the lack of references and research related p

hafeezrm (author) from Pakistan on January 30, 2012:

Thanks Manish for your comments.

hafeezrm (author) from Pakistan on January 30, 2012:

Thanks Manoj Kumar Srivastav for your comments. Your country is beautiful. I have been there enjoying places like Kathmandu, fish-tail mountain, Chitwan Park and many other places.

Manoj Kumar Srivastav on January 30, 2012:

Thank A lot for your paper DM 6 points. I impress very much i am a chartered account located in Nepal.

manish on January 30, 2012:

well thank you very much sir for this concept as it helped me for my exam to understand easily all the concepts,thank you

hafeezrm (author) from Pakistan on January 14, 2012:

Thanks Naima for reading my article.

naima on January 14, 2012:

thans a lot

hafeezrm (author) from Pakistan on December 21, 2011:

Thanks @Macmorrison for your comments. I have written some articles on Methods of Business Research which includes Market Research. You may start with

https://hubpages.com/education/Methods-of-Business...

Macmorrison on December 20, 2011:

It came at the appropriate time for it. The topic was well researched and the criterias were of clarity and simplified. Thank u Sir. But, could u please Sir, assist me on a problem in marketing field?

hafeezrm (author) from Pakistan on November 30, 2011:

Thank you @xuanniecxian for going through my article.

As explained, relevant and irrelevant costs depend on the situation. If it is a simple investment, cost of funds or opportunity cost would be relevant. If any charges are to be paid after buying the investment, these charges would be relevant. Irrelevant would be prepaid insurance or other costs which have already been incurred to bring the investment for sale such as improvement ( in case of house, it could be painting, floor cleaning, replacement of broken items.)

xuanniecxian on November 30, 2011:

sir...how to answer "explain the main priciples used to differentiate between relevant and irrelevant costs for investment appraisal".thank you.

hafeezrm (author) from Pakistan on November 13, 2011:

Relevant cost has been explained above.

Differential cost is the differece between costs of two alternate opportunities. Suppose, you have a plot of land and are now considering whether to put up a textile unit or an edible unit. The cost of land is irrelevant to this decision, it is the differential cost that matter. Suppose the textile unit takes up Rs.500 million whereas the edible oil can be setup with 150 million. The differential cost would be 500 - 150 = 350. It would be relevant cost for this decision.

chandru on November 12, 2011:

thank you sir for the inormation and also i want the difference b/w Relevent cost and Differential cost..

hafeezrm (author) from Pakistan on November 05, 2011:

Thanks Marie Andree for your comments.

Relevant means 'appropriate' or 'suitable' to a particular decision. Suppose you have a piece of land. You are now thinking whether to make a hospital or a university. The cost of land is irrelevant to this decision. Whether you make a hospital or university, the same land will be used in both the cases. But if you are thinking of swapping this land with some other piece of land, the cost of land would be relevant.

Short term decisions are small and routine decisions or administrative decisions or operational decisions. As against this, there are long term decisions or strategic decision. Both have different time horizons.

Marie Andrée on November 05, 2011:

Thank you sir for your articles! but I want to know what is meant by the terms relevant and irrelevant costs in decision-making?

2. Can you identify relevant costs for decision-making and their characteristics

3. Help me to identify and to explain short-run decisions. Thank so much

hafeezrm (author) from Pakistan on October 06, 2011:

Thanks Tania for your comments.

hafeezrm (author) from Pakistan on October 06, 2011:

Thanks share market tips for your comments.

tania on October 06, 2011:

your article is so much knowledgeable. So thank u so much sir

share market tips on September 30, 2011:

I absolutely adore reading your blog posts, the variety of writing is smashing.

This blog as usual was educational, I have had to bookmark your site and subscribe to your feed in i feed.

Your theme looks lovely.Thanks for sharing.

Share Market Tips

hafeezrm (author) from Pakistan on September 27, 2011:

Production costs are computed using a number of techniques such as traditional costing, ABC and ABC-EVA.

hafeezrm (author) from Pakistan on September 27, 2011:

Thanks @Nordose for your comments.

sindhu on September 26, 2011:

dear sir

can u tell me production cost and irs method

Nardose on September 09, 2011:

I am pleasant for your writing

hafeezrm (author) from Pakistan on August 23, 2011:

As the title imply, one is dealing with financial

accounting while the other with cost accounting. So these two are different positions. But there is no hard & fast rule, titles may differ for the same position.

shashike on August 23, 2011:

Dear sir

can you tall me is management Accountant and General manager both are same

lynpearlph on July 02, 2011:

It's a very nice article on my review in CPA board exam. it help me a lot in understanding relevant costs. thanx a lot. More power!!!

Que on April 20, 2011:

Sir , could help me please , what is example of relevant cost actually ?

BARNABAS MACERLINO on February 23, 2011:

Good and simplified

osama kettaneh on January 27, 2011:

hi for all

i wanna to add something,the base in decision making is(CM&NOI)

VC....CM

FC....NOI

thanks for all

Amin Shaikh on January 17, 2011:

Assalam Allaikoom,

I am preparing project for my college and its really helped us thanks for your support.

ann on November 08, 2010:

I truly love this page it gives very important information and answers to question please keep up the good work

Sarah on September 09, 2010:

This really cleared up some questions I was having and helped me a great deal. Thanks!

Samandari on August 07, 2010:

Clear explanations with comprehensible examples. Less Jargon. Good approach

Marion Masango on July 28, 2010:

Great work thanks for the information!

Emmanuel Eze on July 18, 2010:

A great treatise that has helped me in my accounting(elect)course indeed.Keep up the good work.Thanks Sana!!!

varman on June 16, 2010:

10Q 4 information.....

Accounting firm on January 01, 2010:

More good informations thanks for helping me out. Always a pleasure to see information that is useful, thanks again